The draft is due in an hour. Legal has comments. The CFO wants the headline to lead with numbers. The CEO wants “confidence” and “momentum.” Investor relations wants a version for the wire, a version for the website, and a version that won't create problems on the earnings call. That's the moment when an investor relations press release stops being a routine writing task and becomes a governance document.

Handled well, it gives investors a clear record of what happened, why it matters, and how management wants the market to interpret it. Handled poorly, it creates avoidable confusion, raises credibility questions, and weakens the company's message before the first analyst note is even written. The problem gets worse when teams treat every material announcement the same way. Quarterly earnings need one structure. A financing, acquisition, leadership move, or strategic partnership needs another.

That distinction matters more than many teams realize. Companies also need the discipline behind the message. If guidance and assumptions are loose internally, the release will usually show it. Communications leaders who want stronger market narratives often benefit from tightening the underlying planning process first, which is why resources on master forecasting accuracy can be useful well before the drafting stage begins.

Table of Contents

- The High Stakes of Financial Storytelling

- Strategic Foundations and Regulatory Guardrails

- Crafting the Message Anatomy of a Powerful IR Release

- Navigating the Internal Approval Workflow

- Timing Targeting and Distribution Channels

- Post-Release Measurement and Ongoing Dialogue

The High Stakes of Financial Storytelling

A routine product announcement can survive a fuzzy headline or an overworked quote. An investor relations press release usually can't. It sits at the intersection of disclosure, market perception, and corporate credibility. Investors, analysts, journalists, employees, and counterparties may all use the same document to understand what the company is saying officially.

That's why the best teams treat financial storytelling as disciplined translation. They don't write to sound impressive. They write so a busy analyst can scan the release, find the facts, and understand management's position without guessing. The writing has to carry weight under pressure.

A weak release usually fails in predictable ways:

- It hides the lead: Material numbers or key strategic development appear too late.

- It mixes messages: Earnings language gets jammed into a transaction announcement, or vice versa.

- It overstates confidence: Readers see spin where they expected disclosure.

- It lacks context: Raw figures appear without enough explanation to interpret them.

Practical rule: If a skeptical analyst can't summarize the news accurately after one read, the release isn't finished.

The pressure is highest when the news is mixed. Strong revenue paired with margin pressure. A financing that improves flexibility but raises dilution questions. A strategic transaction that sounds promising but won't affect results immediately. In those moments, the release has to do two jobs at once. It must state the facts plainly and frame them responsibly.

This is why seasoned communications leaders insist on precision before polish. Market trust is built less by elegant wording than by clear disclosure, disciplined structure, and the absence of gamesmanship.

Strategic Foundations and Regulatory Guardrails

The hard part often starts before anyone opens a draft. A CEO wants to announce an acquisition. Finance is focused on purchase price allocation. Legal is focused on disclosure risk. Investor relations wants to know the first question analysts will ask at 8:31 a.m. If those threads are not aligned early, the release will read like three documents stitched together.

Material news needs a single standard

An investor relations press release is a disclosure document first and a messaging document second. That order matters because the market will judge the company on completeness, consistency, and timing before it gives management credit for polished language.

The operating rule is straightforward. If a reasonable investor could use the information to make a decision, the company should treat it as potentially material and route it through one disciplined disclosure process. In practice, I want four functions aligned before drafting gets serious: investor relations, legal, finance, and the executive owner of the news.

They need one shared answer to three questions:

- What is the news, in one sentence?

- Why does it matter now?

- How will every investor receive it fairly and at the same time?

Weak alignment shows up fast. Legal starts narrowing language to control liability. Finance adds detail without narrative order. Executives push for emphasis that sounds promotional. The result is technically correct but hard to trust.

Good guardrails prevent that drift:

- Set the source of truth early: Confirm the approved numbers, transaction terms, outlook language, and spokesperson quotes before layout and drafting rounds begin.

- Choose the disclosure path before the wording: Press release timing, investor website posting, exchange requirements, webcast plans, and internal notification should be coordinated as one package.

- Apply the same standard to private conversations: If management wants to explain a point to one investor because it affects valuation, that point likely belongs in the public materials.

Reg FD sits in the background of all of this. Public companies do not get extra credit for being fast if the disclosure process is uneven.

Earnings releases and strategic announcements are not interchangeable

This distinction is where many newer communications leaders get into trouble. An earnings release and a strategic investor announcement may share a distribution list, but they do not serve the same investor need and should not be built from the same template.

An earnings release answers a recurring question: how did the business perform this period, and what changed in the financial profile? A strategic announcement answers a different one: what happened at the corporate level, why does it matter, and what should investors reassess because of it?

That difference affects structure, labeling, approval, and tone. If a financing, acquisition, leadership change, restructuring, major contract, or guidance revision is written like routine quarterly reporting, investors can miss the point or misread the significance. If earnings are written like a splashy corporate announcement, management can look like it is trying to distract from the numbers.

A practical comparison helps:

| Release type | Primary reader question | Best lead | Main risk if mishandled |

|---|---|---|---|

| Earnings release | How did the company perform this period? | Key financial results, major drivers, and outlook context | Burying the numbers or obscuring what changed operationally |

| Strategic announcement | What corporate event occurred and why does it matter? | The event, the immediate investor relevance, and any material terms | Letting readers mistake it for routine reporting or overstate near-term impact |

The trade-off is real. Separate frameworks take more effort. They usually require different checklists, different executive prep, and different legal review priorities. They also produce cleaner market understanding, which is worth far more than the extra hour saved by forcing every event into one generic format.

For teams building those frameworks from scratch, these financial press release writing examples and templates can help standardize structure without flattening important differences between earnings news and strategic disclosures.

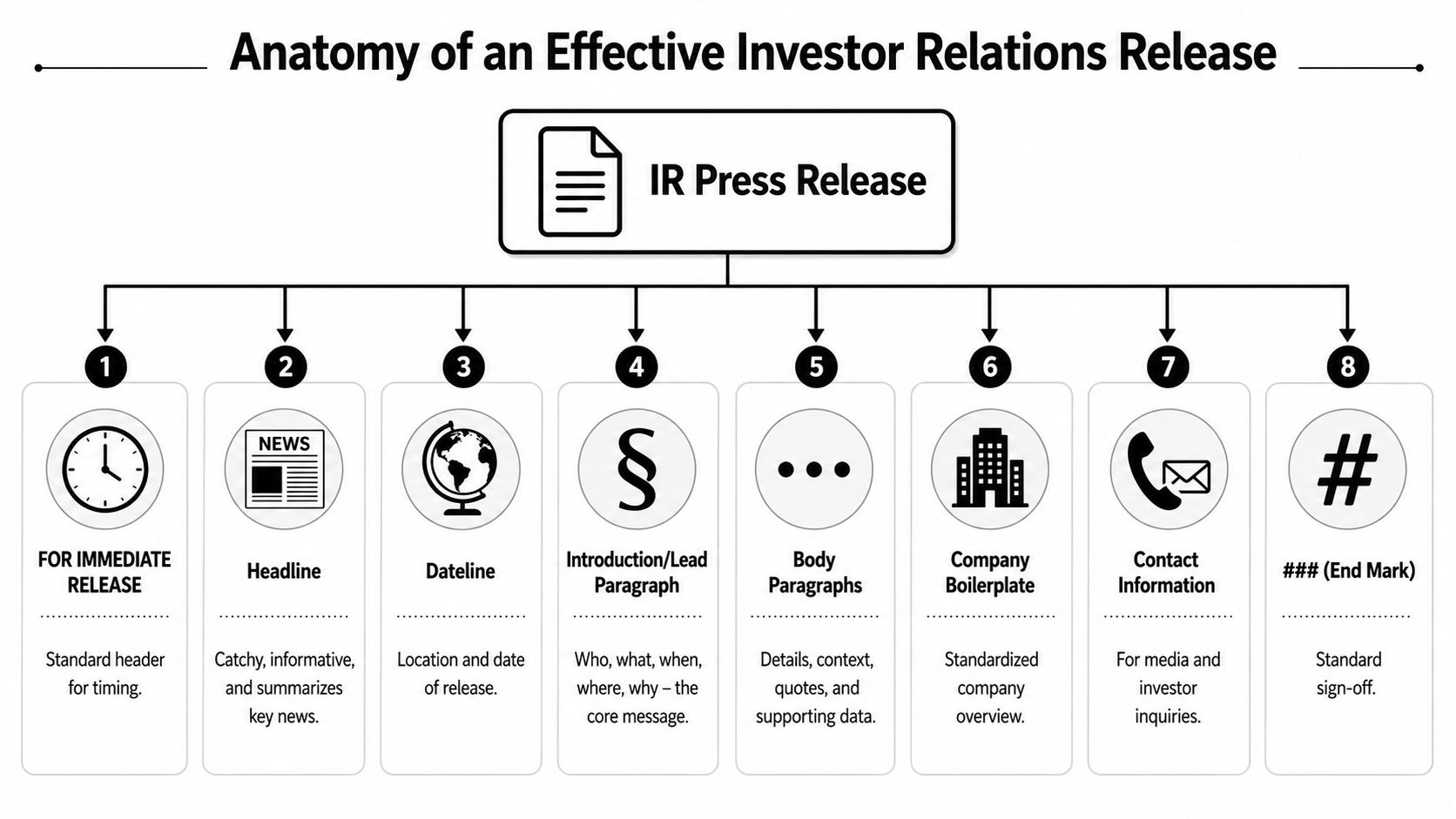

Crafting the Message Anatomy of a Powerful IR Release

A release often succeeds or fails in the first 20 seconds. A portfolio manager opens the email on a phone between meetings. A sell-side analyst scans the headline before deciding whether to read now or after the close. If the release does not signal the type of news immediately, the company creates confusion it then has to spend the rest of the day correcting.

Write the headline for the specific event

The headline is not a branding line. It is a sorting tool for the market.

For an earnings release, lead with period performance and the few figures that frame the quarter correctly. For a strategic announcement, lead with the transaction or corporate event and the fact that makes it material. That distinction matters. If an acquisition, refinancing, leadership change, or guidance revision is written with generic quarterly language, readers can misclassify the news before they reach the first paragraph.

A strong headline usually does three things:

- Names the event clearly: earnings results, acquisition, financing, divestiture, leadership change, guidance update, or another material development.

- States the investor-relevant fact: revenue growth, margin pressure, deal value, expected proceeds, board approval, closing status, or another concrete point.

- Stays factual: investors trust specificity more than promotional wording.

“Company Announces Strong Quarter” forces the reader to do extra work. “Company Reports Second Quarter Revenue Growth of 12% and Reaffirms Full-Year Guidance” tells the market what happened and why it matters. Strategic news follows the same rule, but the lead fact may be the agreement signed, capital raised, asset sold, or executive appointed.

Build the body for scan speed and diligence review

The body has two jobs. It has to help a fast reader get the point immediately, and it has to hold up when an analyst, lawyer, or journalist reads every line closely.

That usually means writing in layers. Start with a lead paragraph that states the news cleanly. Follow with highlights that surface the facts readers are most likely to quote. Then use the remaining space to explain drivers, terms, timing, and limits.

A workable structure looks like this:

- Lead paragraph: State the company name, the event, and the immediate investor significance.

- Key highlights: Present major figures, terms, milestones, or conditions in a format that is easy to scan.

- Management quote: Add judgment and strategic rationale. Do not repeat numbers already shown above.

- Supporting detail: Explain what drove the results or how the transaction changes capital structure, operations, or outlook.

- Boilerplate and contacts: Direct investors and media to the right follow-up paths.

For teams that want a starting point, these financial press release writing examples and templates are useful for pressure-testing structure before legal review.

One test I use is simple. If an analyst asks, “What is the one thing I should update in my model or thesis after reading this?” the release should answer that question without forcing them to hunt.

Keep management quotes disciplined

Weak IR quotes waste valuable space. They restate the headline, add broad optimism, and avoid the issue that matters to investors.

A useful executive quote does one of three things: explains the operating driver behind the numbers, clarifies the strategic logic of the announcement, or frames what management expects investors to watch next. If the quarter was mixed, the quote should acknowledge that mix. If a deal has conditions or integration risk, the quote should not pretend those trade-offs do not exist. Credibility usually improves when management sounds precise rather than enthusiastic.

Use one framework for earnings and another for strategic announcements

Many teams lose clarity when they use one generic template for every release.

Earnings releases work best when the narrative starts with period performance, then explains drivers, then addresses outlook. Strategic announcements need a different sequence because the reader is asking a different question. The most reliable order is:

- What happened

- Why the company did it

- What changes now

- What investors should monitor next

That framework keeps strategic releases from sounding like soft corporate PR. It also reduces the risk that material details get buried below broad positioning language.

If some terms are confidential, contingent, or still subject to approval, state that directly. Say what is known, what remains pending, and what the company cannot yet disclose. Investors can handle uncertainty. They react poorly to ambiguity that looks deliberate.

Formatting helps, but only after the writing does its job. Tables, bullets, and design elements can improve readability. They cannot rescue a release that never explains the economic substance of the news in plain text.

Navigating the Internal Approval Workflow

At 4:07 p.m., the CFO approves one draft, legal marks up another, and the version sent to the wire still carries an outdated metric in the headline. The market does not care which internal handoff failed. It sees a company that looks loose with its own disclosure.

A clean process protects the company

An approval workflow is a disclosure control. It is also a message discipline tool. I have seen strong releases weakened late in the process because five reviewers tried to rewrite the same paragraph for different purposes.

The fix is simple in concept and hard in practice. Name one document owner. That person controls the master file, resolves comment conflicts, and verifies that every figure ties back to the approved source. Without that role, teams spend the final hour comparing versions instead of checking substance.

The review path should match the type of announcement. Routine earnings releases usually move through a repeatable sequence because the core disclosures and supporting schedules are familiar. Strategic investor announcements need tighter scrutiny on rationale, contingencies, approvals, and what remains unknown. Using the same approval rhythm for both often creates either delay or under-review.

A workable process usually includes:

- One source file: Keep drafting in a single controlled document, not scattered email attachments.

- Named owners for key decisions: Every material edit should have a responsible reviewer.

- A fixed review order: Finance checks numbers first, legal reviews disclosure and phrasing, IR tests investor clarity, executives confirm position, and communications prepares the final package.

- A release readiness check: Confirm headline, dateline, contacts, links, attachments, IR website posting, and any supporting decks or webcast references.

Who signs off and what they own

Internal approvals fail when reviewers are not clear on scope. Finance should not be recasting the lead quote for style. Communications should not be redefining non-GAAP terms. Legal should not be the first team checking whether the release answers the investor question.

| Role | Primary responsibility |

|---|---|

| Finance or CFO office | Confirms figures, definitions, and consistency with formal reporting |

| Legal counsel | Reviews disclosure risk, material statements, and fair presentation |

| Investor relations | Tests whether the release answers investor questions clearly |

| CEO and senior leadership | Aligns tone with company position and strategic intent |

| Communications | Owns readability, structure, distribution readiness, and final packaging |

For earnings releases, I recommend a short final checklist tied to the reporting package. For strategic announcements, add a second checklist that asks different questions: What approvals are still pending? What conditions could change the outcome? What investor misunderstanding is most likely if someone only reads the headline and first three paragraphs?

That distinction is easy to miss, and it matters.

Formatting choices should also survive the review process if they improve comprehension. Bullets, tables, and subheads often help investors and journalists find the economic point faster, especially in longer strategic releases with multiple conditions or transaction steps.

For teams rethinking ownership, guidance on who should write your press release helps clarify who is accountable for accuracy, not just who can draft clean copy. And before investor email alerts go out, run an email spam test so the release notification reaches inboxes instead of disappearing into filters.

Timing Targeting and Distribution Channels

At 4:03 p.m., the earnings release hits the wire. At 4:07, the investor deck is still missing from the IR site, a reporter posts an outdated revenue figure from an earlier draft, and analysts start emailing questions that should have been answered in the first package. The problem is not only timing. It is channel control.

That risk looks different for routine earnings releases than it does for strategic investor announcements. Earnings news usually follows a known cadence, with investors expecting the release, the deck, and the webcast details in a familiar order. Strategic announcements such as acquisitions, divestitures, financings, leadership changes, or revised guidance need tighter message control because readers are often seeing the issue cold and forming a view from the headline alone.

Channel choice changes how the news lands

An investor relations release should publish through a coordinated set of channels, with one version serving as the clear reference point. The wire gives immediate reach across media systems, terminals, and databases. The investor relations website holds the full record, including supporting materials and any updates. Required filings handle formal disclosure obligations. Email and social distribution should direct people back to the canonical source, not compete with it.

Each channel has a specific role:

- Newswire distribution: Broad, fast visibility across financial media, data platforms, and market participants.

- Investor relations website: Permanent archive for the release, deck, webcast links, and related documents.

- Direct email alerts: Immediate notification for analysts, investors, lenders, and journalists already following the company.

- Corporate social channels: Useful for reach and amplification, but not the place to carry the full substance of material news.

For teams building the distribution plan, how to distribute press release gives a practical checklist for sequencing channels and assets.

Timing and packaging shape reception

Release timing should match the type of announcement. For an earnings release, consistency usually matters most. Publish on the cadence investors know, make sure the deck and webcast details are live at the same time, and avoid small sequencing errors that create unnecessary questions about controls. For a strategic investor announcement, timing is more situational. The right window depends on board approvals, filing readiness, market hours, transaction conditions, and how much context investors will need in the first read.

Packaging should follow the same logic. A routine earnings release can stay tighter because the market already knows the format and will often look to the tables, deck, and prepared remarks for detail. A strategic announcement usually needs more explanation up front, especially if the event changes capital allocation, guidance, ownership, leadership, or the company's risk profile.

Use visuals carefully. A chart, deal structure graphic, or timeline can improve comprehension if it answers a real investor question faster than text would. If it adds polish without clarity, leave it out.

I usually tell teams to edit for decision-useful information, not word count. Some earnings releases work well as short documents because investors know where to look for the numbers. Strategic releases often need more room to explain terms, approvals, expected timing, and what remains uncertain. The better rule is simpler. Put the material facts in the release, then let the deck, FAQ, or webcast handle the supporting explanation.

A good IR package gives every audience the same core facts, while letting each channel do its own job.

Email distribution also deserves operational attention. If alerts go to investor and media lists, inbox placement affects who sees the news promptly and who sees it late. Before a high-stakes send, teams often run the message through an email spam test to catch authentication, formatting, or deliverability problems that can delay visibility at the worst possible moment.

Post-Release Measurement and Ongoing Dialogue

The wire hits at 8:00 a.m. By 8:20, the stock is active, reporters have pulled their headline angle, and IR is already fielding the same two questions. That first half hour often tells you whether the market understood the announcement or whether the company now needs to spend the day correcting preventable confusion.

Measure more than pickup

Start with the obvious indicators. Review media coverage, investor site traffic, inbound questions, analyst notes, and the topics that surface in early outreach. Those signals show whether the release framed the story correctly.

The measurement approach should match the type of announcement. A routine earnings release is usually judged on accuracy, consistency with prepared remarks, and whether analysts found the numbers and drivers quickly. A strategic investor announcement needs a broader read. Teams should test whether the market understood the rationale, timing, approvals, risks, and impact on capital allocation or guidance. Mixing those two scorecards is a common mistake, and it can hide message problems until the next call.

The most useful post-release indicators are usually directional, not flashy:

- Which points journalists led with in their first coverage

- Which investor questions repeated across calls and emails

- Whether analysts focused on the issue management intended to highlight

- Which supporting assets drew the most attention after the release

- Whether social and market commentary reflected the company's framing or challenged it

For communications teams that want a cleaner view of competitive visibility after a release, MyMentions' SOV calculation strategies can help frame share-of-voice analysis more rigorously.

Treat the release as the opening move

A release starts the dialogue. It does not finish it.

If IR gets immediate questions on a point that legal thought was clear, revise the FAQ, prep management, and decide whether the website or webcast remarks need added context. If journalists skip the message the company cared about, that usually means the release buried the implication or failed to explain why the news matters now. I advise teams to log these patterns the same day, while the gaps are still obvious and before internal retellings smooth them over.

A disciplined same-day debrief helps. Communications, investor relations, legal, and the relevant executives should compare what they intended to signal with what each audience heard. For earnings news, the goal is usually to confirm alignment across the release, tables, deck, and call script. For strategic announcements, the goal is often different. Check whether the market understood the decision logic, what is confirmed, what still depends on approvals or closing conditions, and what management is not yet in a position to promise.

Trust builds over repeated cycles. Investors remember whether follow-up answers match the release, whether management addresses difficult points directly, and whether later actions support the original message.

If a team needs practical help with structure, templates, and distribution planning, Press Release Zen is a useful resource for building cleaner press release workflows and reducing avoidable mistakes before material news reaches the market.